Japan

Japan

The Road to 2050: Risks and opportunities in sustainability-linked products

February 10, 2022

-

3 minutes

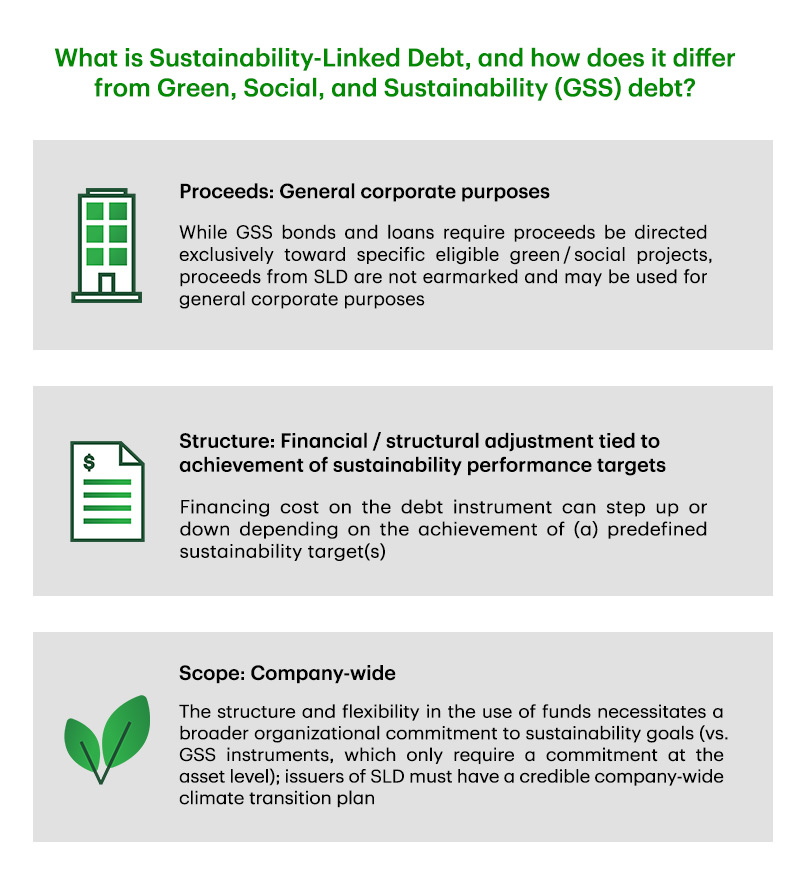

Sustainability-linked debt (SLD) is the newest and fastest growing segment of sustainable capital markets. SLD has emerged as a popular financing mechanism for corporations worldwide to demonstrate their accountability and commitment to sustainability. These products are characterized by flexible use of proceeds and linked to the achievement of predetermined sustainability objectives.

What's driving the growth of this market?

From 2020 to 2021, sustainability-linked bond (SLB) issuance grew nearly 10-fold from ~US$10B to ~$100B; at the same time, the sustainability-linked loan (SLL) market nearly tripled from ~$130B to ~$375B. Combined, these two products have moved from representing 2% of sustainable capital markets debt in 2017 to 32% in 20211 . Growth in this market can be attributed to:

- Flexibility: In the use of funds; this has opened the market to a wide range of issuers that have historically been excluded from sustainable capital markets, such as those in carbon-intensive or asset-lite sectors.

- Scalability: General corporate purpose use of proceeds enables corporations to issue SLD at scale, unrestricted by volume of qualifying assets.

- Opportunity: Targets generally apply to the entire company and are not limited to specific projects or investments, allowing issuers to demonstrate commitment to their overall corporate sustainability strategy.

- Standardization: The International Capital Markets Association (ICMA) along with other industry associations codified best practices in the Sustainability-Linked Loan Principles (published May 2019; updated July 2021) and Sustainability-Linked Bond Principles (June 2020), enhancing the market's credibility.

- Successful precedents: Recent precedents have demonstrated the robust investor appetite for SLD products, as stakeholders increasingly demand accountability and action on ESG issues from corporations.

What are the key concerns around sustainability-linked debt?

- Funding for general corporate purposes: While flexibility in use of proceeds is a benefit to the issuer, some investors prefer that their funds be directed to specific green/social projects.

- Achievement of targets: Issuers must be comfortable with the potential reputational and financial risks of missing their target(s).

- Investors / lenders profiting from missed targets: Concerns around capital providers earning a premium payment when companies fail to meet their sustainability objectives.

Another concern is the potential for 'greenwashing': where the credibility of targets or the structure of the bond/loan lacks ambition. Some common pitfalls in this area include:

- One or more targets have already been met, or are not material or not ambitious, or are not appropriately weighted based on materiality and ambition.

- Baseline for goals is not representative or is unreasonably far in the past.

- Financial penalties are not material.

Where is the market heading and what needs to happen next?

Every sector could do more to reach their environmental aspirations and SLD offers an attractive avenue for many companies to finance these ambitious goals. Investors need to be well-educated on the difference between use of proceeds and sustainability-linked debt instruments to have a balanced view of the benefits and considerations. As the SLD market continues to grow, it is important that rigorous standards are upheld to maintain market credibility and ensure maximum impact.

1Source: Bloomberg. Note: All figures in US$ unless otherwise stated.

Read another insight from our The Road To 2050 series – Developing voluntary carbon markets