Japan

Japan

Bank Crisis Moves Overseas – ETNs Back Under the Microscope

By: Andres Rincon

March 28, 2023 - 3 minutes 30 seconds

The U.S. bank crisis was first concentrated on regional banks lacking a diversified client base or asset mix, but it now appears to be taking on a global nature and putting larger banks under the radar. Although the structure of exchange-traded funds (ETF) is well sheltered from the bank crisis given that all assets are segregated and owned by its investors, the same cannot be said of all Exchange Traded Product (ETP) structures. Exchange Traded Notes (ETNs) are unsubordinated and unsecured debt securities of the note's issuer, most of which are banks, and have come back again under the microscope.

European banks are now seeing their equities and bonds under pressure. Recently, share prices for a major global investment bank based in Switzerland dropped nearly 25% after its largest investor said it would not increase its stake. The bank's CDS price reached crisis levels as investors rushed to buy protection. The Swiss National Bank, the central bank of Switzerland, provided a loan of CHF 50BN, but this intervention did not stop a deposit exodus with outflows of CHF 10BN during the week. The situation was so compromised that the Swiss government initiated a fast-track acquisition for it by another Swiss bank.1

A closer look at ETNs

Although ETFs have minimal exposure to the Swiss bank's demise, the ETN structure can have significant exposure to it as a note issuer. ETNs are exchange traded securities but are slightly different in that they are unsubordinated and unsecured debt securities of the issuer. They are similar to a bank-issued corporate bond with an expiry (no payment of interest). However, ETNs trade on an exchange and track an index of securities, commodities or any other tradeable security.

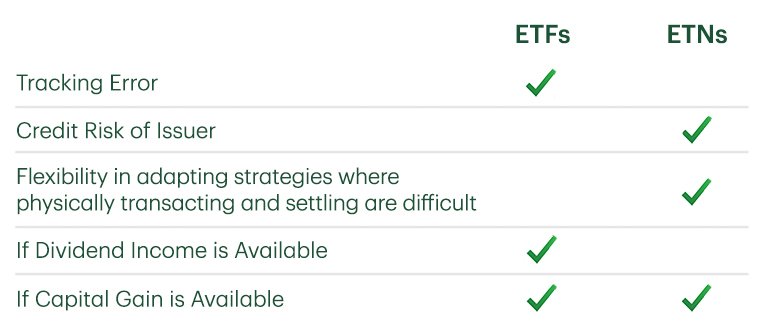

One of the key risks of ETNs is that they carry credit risk from the issuer of the ETN, as the investor does not own the assets within the ETN, but rather owns a promissory note from the issuing bank to deliver the return of a benchmark. In the case of a bank default (as was nearly the case), ETNs issued by this bank could be at risk.

The advantages of ETNs

ETNs offer several advantages in exchange for this risk. The first is flexibility in strategies. ETNs allow strategies where physically settling the underlying securities each day is difficult. As long as a price discovery process exists, ETNs can be based on an index. This ability allows complex investments or those that are difficult to manage via an ETF to become investable through an ETN. Unlike some ETFs, ETNs do not have tracking error risk because the issuer promises to pay the exact return of an underlying index. It's also worth noting that all gains are considered capital gains.

So, are global ETNs okay?

As the bank crisis spilled into Europe, the inherent credit risk increased for over US$600mm of ETNs issued by the failing Swiss bank. If it had fully gone under and not been acquired, many of these ETNs could have been caught up in the proceedings. Investors may need to go to court to recoup any value from these ETNs. Even so, ETNs might not yet be out of the woods, and whether these ETNs will continue to exist or be unwound is yet to be determined.

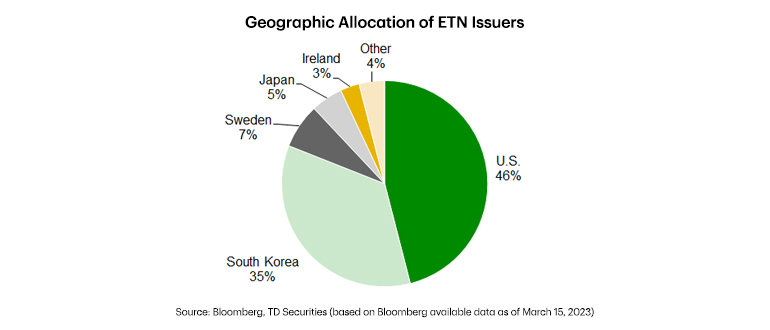

Many top banks globally are also involved in the ETN business. In addition to the North America and Europe, South Korea and Japan also have active ETN markets with local issuers dominating the market. However, no North American or European banks are active in the ETN market in South Korea or Japan despite its size. Some European banks have a small presence in Europe, while most banks concentrate their ETN business in the U.S.

In summary:

As the bank credit crisis intensifies and spreads to other regions, the viability and risk of ETNs may continue to be more significant. Many of the top ETN issuing banks were considered systematically important banks too big to fail, but as was recently evident with the collapse a major bank in Europe, the risks to ETNs appear to be higher than many would realize.

- Source: Swiss National Bank: Swiss National Bank provides substantial liquidity assistance to support UBS takeover of Credit Suisse as of 3/19/2023.

Director and Head of ETF Sales & Strategy, TD Securities