Market Leadership

What Do Leading Indicators Tell Us About Canadian Recession Risks?

By: Robert Both

August 18, 2022 - 2 Minutes 30 Seconds

We continue to look for a soft landing in Canada as leading indicators begin to flash red across other parts of the globe. Activity data has held up reasonably well through Q2 and the labour market remains historically tight. However, the shifting global backdrop warrants a closer look at leading indicators for Canada.

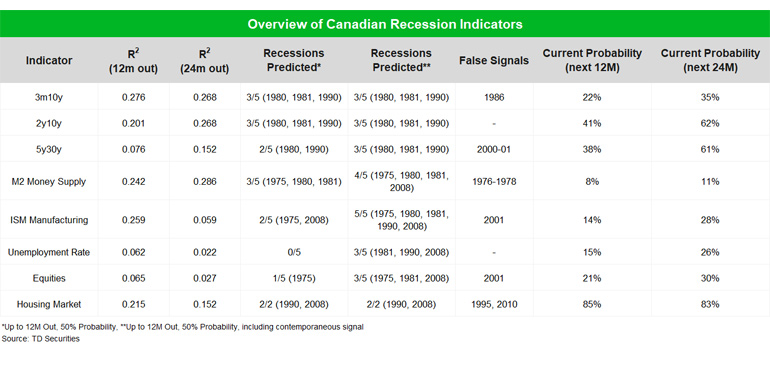

Leading Indicators for Canada

We evaluate several leading indicators and find that yield curves continue to provide the strongest signal ahead of Canadian downturns. Monetary aggregates, the ISM Manufacturing Index, and the housing market also provide some insight as leading indicators, while others like the equity market and the unemployment rate are more useful as a contemporaneous signal.

The current level of Canadian yield curves is consistent with a 20-40% chance of a recession over the next twelve months, or 35-60% probability over the next two years, although other measures such as the ISM Manufacturing Index or labour/equity markets suggest a lower probability. The housing indicator is the most alarming of the group, as it signals an 85% likelihood of recession over the next year or two; although we think this overstates the probability of a downturn, it is also alarming in an environment where residential investment makes up a larger share of total activity than any period since 1990. Overall, we see a 40% probability of a recession over the next 12 months, or 50% probability over the next two years.

Mitigating Factors

It is difficult to discount the likelihood of a near-term recession, especially in light of more tangible signs of slowdown across the US, but there are some mitigating factors that warrant mention. Canada still has a large exposure to the natural resources sector and even though energy demand (and prices) will come under pressure in a global slowdown, it is difficult to envision oil prices returning to 2019 levels in a supply-constrained world. Higher energy prices are no longer the boon they once were for non-residential investment, but they will still bring a positive impact from investment and corporate tax revenues. Canadian demographics offer another mitigating factor given strong population growth (+1.3% y/y in Q2) and international migration. This could result in a scenario where GDP growth is positive, while contracting on a per-capita basis.

The Bank of Canada has stated that the path to a soft landing has narrowed, but strong population growth and natural resources exposure should help to mitigate the likelihood of an outright recession. If activity does contract sharply into year-end (or early 2023), the Bank of Canada may find its response limited by the inflation backdrop; it is difficult to envision a scenario where the Bank does not exceed the upper-limit of its neutral range by October, and we still see a high bar for the Bank to unwind these hikes in early 2023.

The Bank of Canada has stated that the path to a soft landing has narrowed, but strong population growth and natural resources exposure should help to mitigate the likelihood of an outright recession. If activity does contract sharply into year-end (or early 2023), the Bank of Canada may find its response limited by the inflation backdrop; it is difficult to envision a scenario where the Bank does not exceed the upper-limit of its neutral range by October, and we still see a high bar for the Bank to unwind these hikes in early 2023.

Read the full report: What do Leading Indicators Tell us About Canadian Recession Risks

Vice President and Macro Strategist, TD Securities

Vice President and Macro Strategist, TD Securities

Vice President and Macro Strategist, TD Securities