Japan

Japan

Canadian Households Facing a Winter of Discontent

By: Robert Both

October 5, 2022 - 4 Minutes

Canadian households will face intense headwinds into 2023 as a highly leveraged household sector contends with a sharp rise in consumer interest rates alongside the cost of inflation. Households have added nearly $400bn in mortgage debt since the end of 2019, with 5y fixed mortgage rates at historic lows for most of that period, which will make them more vulnerable as those loans are refinanced at much higher rates going forward. We are now starting to see some evidence of higher rates weighing on the household sector, but headwinds will intensify into and throughout next year.

Household Leverage Has Spent Years on the Back Burner

Household leverage has been a vulnerability in the Canadian economy for some time now. Unlike the US, Canadians came out of the Global Financial Crisis with considerably more leverage, and debt-to-income ratios took another leg higher after the Bank of Canada cut rates in 2015. The pandemic followed a similar roadmap, as lower interest rates and generous fiscal transfers provided some cushion for highly leveraged households, but that cushion has since been removed.

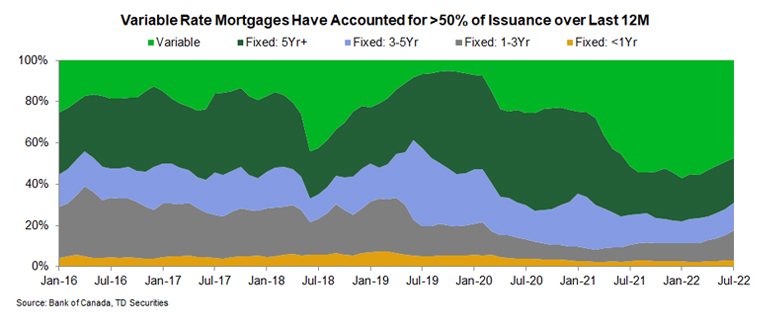

In Canada, 42% of outstanding mortgages were fixed over a term of 5 years (or longer) at origination. This has helped isolate a large portion of Canadian households from the impact of rate hikes over the near-term. Variable rate loans have made up a much larger share of recent mortgage issuance though, accounting for 53% of all mortgage lending over the last 12 months, while the share of 5y fixed issuance has fallen to just 22% from 50% in the early stages of the pandemic. The larger share of variable rate issuance will increase households' sensitivity to higher interest rates at an inopportune moment, with the Bank of Canada now projected to reach a terminal rate above 4%.

In Canada, 42% of outstanding mortgages were fixed over a term of 5 years (or longer) at origination. This has helped isolate a large portion of Canadian households from the impact of rate hikes over the near-term. Variable rate loans have made up a much larger share of recent mortgage issuance though, accounting for 53% of all mortgage lending over the last 12 months, while the share of 5y fixed issuance has fallen to just 22% from 50% in the early stages of the pandemic. The larger share of variable rate issuance will increase households' sensitivity to higher interest rates at an inopportune moment, with the Bank of Canada now projected to reach a terminal rate above 4%.

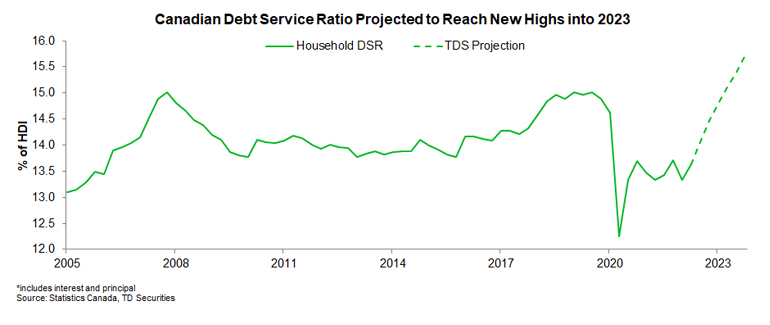

Debt payments accounted for 13.6% of disposable incomes in Q2, up 0.3pp from the prior quarter, but the debt service ratio is still well below the 15% peak from 2019. As the Bank of Canada did not start tightening policy until March, we see this increase as the beginning of a much larger move with the debt service ratio expected to exceed previous highs in 2023.

Breakdown of Household Mortgage Debt

Using some simplifying assumptions, we estimate that 52% of residential mortgages are partially exposed to higher rates over the next twelve months. This includes $489bn in variable rate loans, most of which have fixed payments (to a threshold), alongside 27.5% ($262bn) of outstanding fixed rate mortgages. As the average rate at origination for these fixed loans sits around 3.2%, those renewing fixed rate mortgages over the next twelve months face a substantial interest rate shock.

The implications for variable rate borrowers are more ambiguous, given uncertainty around how many fixed-payment variable loans have hit a trigger point, and how those loans are being treated on an individual level. Some borrowers are facing higher payments, while others are accruing more principal and/or adding to their mortgage term. We can also back out the theoretical buffer built into variable rate loans over 2020-21 using actual variable lending rates; for variable rate mortgages taken out through 2021 when the Bank of Canada was operating at its effective lower bound, this buffer averaged around 3.25%. After 300bps of hikes to date, this suggests most of these loans will require higher payments (or longer amortization periods) after the October BoC decision.

The implications for variable rate borrowers are more ambiguous, given uncertainty around how many fixed-payment variable loans have hit a trigger point, and how those loans are being treated on an individual level. Some borrowers are facing higher payments, while others are accruing more principal and/or adding to their mortgage term. We can also back out the theoretical buffer built into variable rate loans over 2020-21 using actual variable lending rates; for variable rate mortgages taken out through 2021 when the Bank of Canada was operating at its effective lower bound, this buffer averaged around 3.25%. After 300bps of hikes to date, this suggests most of these loans will require higher payments (or longer amortization periods) after the October BoC decision.

Slowdown Coming

The combination of fixed rate mortgage renewals and potential for higher variable rate payments will drive total debt payments sharply higher into next year, with the debt service ratio expected to reach new highs by mid-2023. This, along with the ongoing inflation shock and erosion of household confidence, will introduce a material headwind for the consumption outlook in 2023 and beyond.

We have repeatedly argued that elevated household leverage supports a lower terminal rate in Canada vs the US, and the headwind to consumption growth is a key aspect of that view. US households spent just 9.6% of their disposable incomes servicing debt in Q2, ~30% lower than the Canadian DSR, and also carry less leverage than Canadian households; while rising interest rates will also bite into the US growth outlook, Canadian households should prove more sensitive to restrictive policy rates.

This environment sets the stage for the Bank of Canada to pivot to a more dovish stance in the coming quarters. We look for the Bank of Canada to keep hiking through January 2023, but the expected deterioration in economic data will make for a more difficult environment to lift rates beyond that. Similarly, as pressure builds on Canadian households through the first half of 2023 and growth stalls, the Bank of Canada is unlikely to hold rates above 4% for an extended period. With GDP growth expected to fizzle out in the first half of 2023 and inflation trending back towards the upper half of the Bank's target range by H2, we expect the pivot to come relatively quickly after the last hike, with quarterly rate cuts starting in 2023Q3.

We have repeatedly argued that elevated household leverage supports a lower terminal rate in Canada vs the US, and the headwind to consumption growth is a key aspect of that view. US households spent just 9.6% of their disposable incomes servicing debt in Q2, ~30% lower than the Canadian DSR, and also carry less leverage than Canadian households; while rising interest rates will also bite into the US growth outlook, Canadian households should prove more sensitive to restrictive policy rates.

This environment sets the stage for the Bank of Canada to pivot to a more dovish stance in the coming quarters. We look for the Bank of Canada to keep hiking through January 2023, but the expected deterioration in economic data will make for a more difficult environment to lift rates beyond that. Similarly, as pressure builds on Canadian households through the first half of 2023 and growth stalls, the Bank of Canada is unlikely to hold rates above 4% for an extended period. With GDP growth expected to fizzle out in the first half of 2023 and inflation trending back towards the upper half of the Bank's target range by H2, we expect the pivot to come relatively quickly after the last hike, with quarterly rate cuts starting in 2023Q3.

Vice President and Macro Strategist, TD Securities