It All Looks So Different This Time

By: Mario Mendonca

December 8, 2022 - 5 minutes

The Sweet Spot: Bloated Balance Sheet with Expanding Margins

The group's Liquidity Coverage Ratio (LCR; the proportion of highly liquid assets) expanded abruptly early in the pandemic as QE drove deposits higher, but loan growth did not keep pace. Now we see LCRs trending lower, as deposit growth slows (even starts to run-off) and loan growth accelerates.

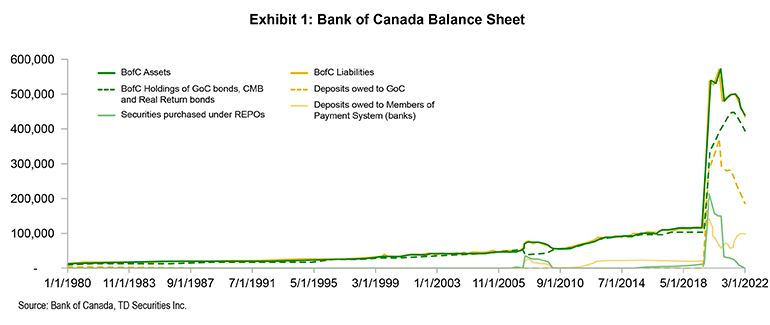

The vast increase in the Bank of Canada's balance sheet

We view the REPOs (repurchase agreements) as a quick shot of adrenalin to the system, and the significant bond holdings as the "real" quantitative easing (QE).

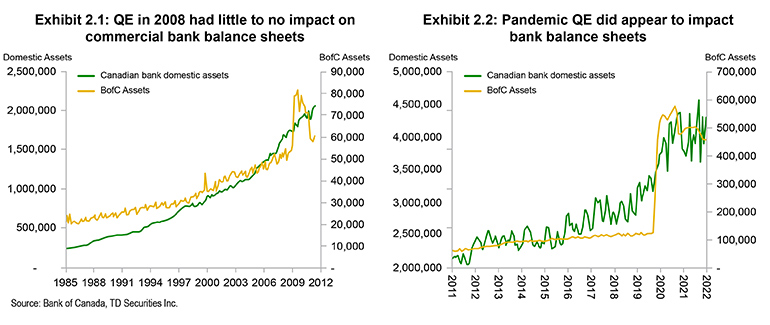

The impact of pandemic QE on bank assets

Why was the effect of the Pandemic's QE different?

We contend that QE in 2020 was different from QE in 2008 in that the central banks purchased assets outside the commercial banks.

What have we learned so far?

- In QE, central banks, through purchases of securities from commercial banks, increase reserves at the banks – creating more liquidity.

- In pandemic QE, central banks purchased securities outside the banking sector which created deposits within the banking sector. The banks are sitting on significantly more assets and deposits in Canada and the U.S. than they were before the pandemic.

What happened next?

How did QT increase liquidity ratios?

Shortly after the pandemic commenced, QE drove deposits materially higher, the proceeds of which were invested in HQLA (high quality liquid assets) and other liquid assets, driving the LCR (Liquidity Coverage Ratio) much higher. Note that the LCR is a consolidated measure. That is, the capital ratios (discussed above) and liquidity ratios include the U.S. and other non-Canadian operations of Canada's banks.

The banks are in a sweet spot – Higher margins earned on bloated balance sheets

When we say the banks are in a sweet spot, what we mean is margins are climbing, while balance sheets remain bloated driving unusually strong Net Interest Income (NII). But nothing lasts forever. What caused the balance sheets to become bloated in the first place, could well shrink bank balance sheets going forward. To be very clear, this has already commenced in the U.S. – declining deposit balances and higher deposit betas.

If we do in fact see average earning assets flatline over the next few years, capital allocation – buybacks, U.S. deals, and acquisitions more generally, would play an outsized role in how investors look at the individual banks.

Subscribing clients can read the full report on the TD Securities Market Alpha Portal

Managing Director and Senior Financial Services Analyst, TD Securities

Managing Director and Senior Financial Services Analyst, TD Securities

Managing Director and Senior Financial Services Analyst, TD Securities